The 50-Year Mortgage: A “Solution” That Solves Nothing

It’s hard to scroll through social media these days without running into flashy financial “gurus” offering bad advice in bite-sized videos. Some claim buying a home is a mistake — even as they personally own thousands of rental units. The irony is real.

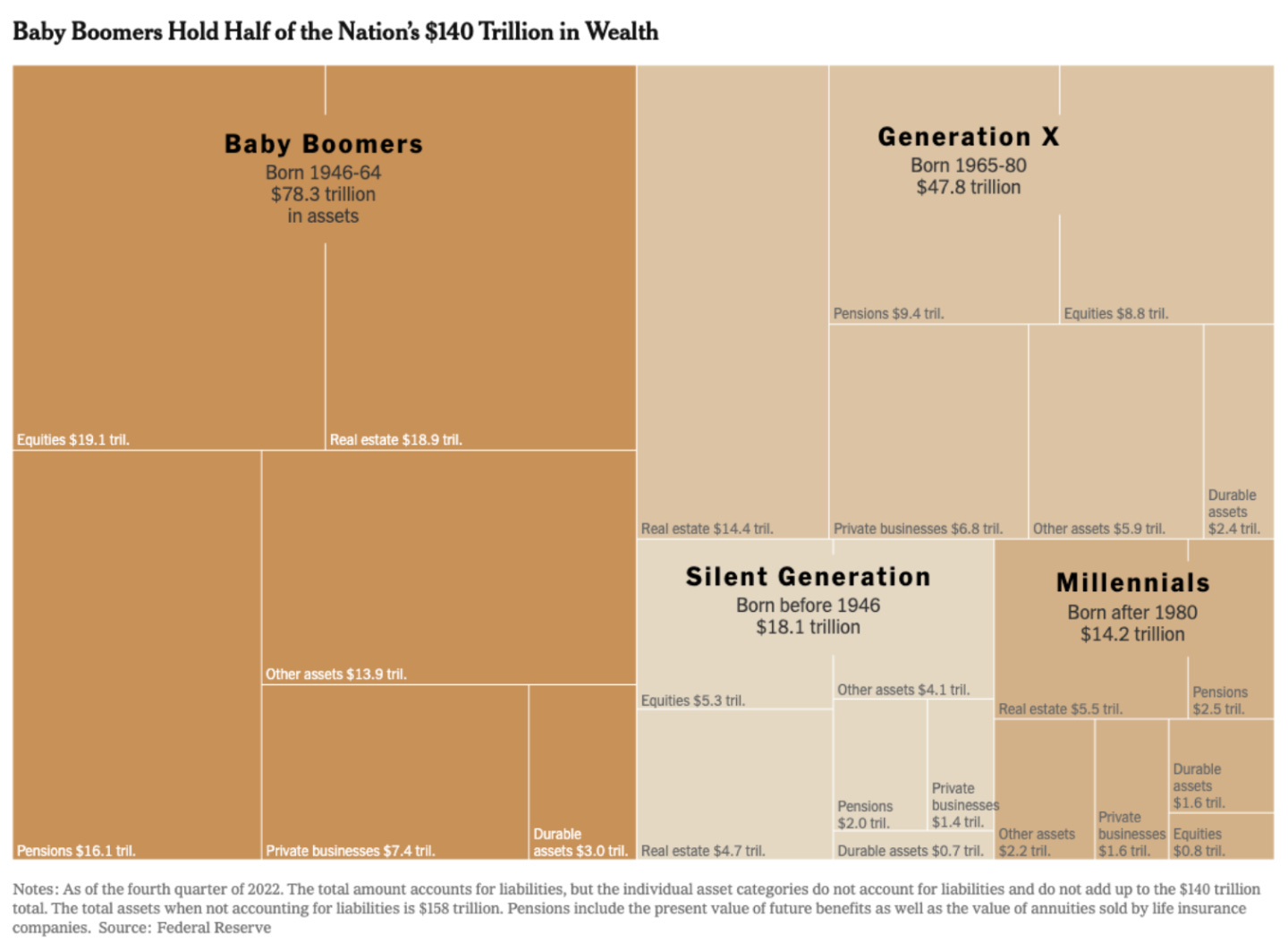

But behind all the noise, something serious is happening: the largest transfer of wealth in human history. According to The New York Times, Baby Boomers currently hold about half of the nation’s $140 trillion in wealth, and much of that is in real estate — around $18.9 trillion worth. That wealth is starting to shift to younger generations.

Source: The New York Times

Unfortunately, there’s a new idea floating around that could make that transfer much harder: the 50-year mortgage. Let’s break down why that’s such a bad deal.

The Math Doesn’t Lie

At first glance, a 50-year mortgage sounds appealing. The payments are stretched out longer, which means lower monthly bills, right? Well, not really.

Take a $1,000,000 loan at 6% interest:

15-year mortgage: about $8,500/month

30-year mortgage: about $6,000/month

50-year mortgage: about $5,700/month

That’s less than a $300 monthly difference between the 30-year and 50-year loans. But here’s the catch — that small “savings” comes with a massive long-term cost.

If you held the loan to term, here’s what you’d pay in interest alone:

15 years: $519,000

30 years: $1.16 million

50 years: $2.2 million

So who benefits from this kind of deal? The bank. Not the homeowner, and certainly not the next generation trying to build wealth.

The Equity Trap

Most people don’t keep their mortgage for 50 years — or even 30. In reality, Americans move every 5–10 years. If you sell after 10 years, here’s the problem:

With a 15-year mortgage, you could have built around $563,000 in equity.

With a 30-year, about $163,000.

With a 50-year, only $43,000.

That means you’ve lost hundreds of thousands in potential wealth.

What’s worse, that little $300 monthly savings adds up to about $88,000 over 10 years, but it comes at the cost of $120,000 less equity. You didn’t save — you just paid more to the bank and kept less for yourself.

As one KW New Orleans broker put it: “We’re shackling people to poverty.”

Who Really Wins?

The idea behind longer-term loans is to make housing more “affordable.” But in reality, they mostly protect the wealthy and big investment banks. Baby Boomers — many of whom are major property owners — benefit when prices stay high. So do banks and lenders who collect more interest over time.

Meanwhile, buyers get stuck in homes with little to no equity, unable to move up or reinvest in their future.

Lessons for Agents and Clients

Real estate professionals have a responsibility to educate clients about the real math behind big financial decisions. A 50-year mortgage may sound like innovation — but it’s really a long, expensive trap that transfers wealth away from homeowners and into the hands of institutions.

Homeownership is one of the few ways Americans consistently build wealth over time. Diluting that through longer loans only makes it harder for future generations to get ahead.

The takeaway is simple: think long-term — but not that long.

Disclaimer: This post is for informational purposes only and does not constitute financial or legal advice. Always consult a licensed real estate professional or financial advisor before making major real estate decisions.

This article was originally published on our website, which can be accessed here.